Stephen M. Mills, CIMA® Partner

Chief Investment Strategist

There is an old adage most everyone is familiar with that warns about the consequences of someone’s desires, “Be careful what you wish for.” In our January 2025 Investment Outlook & Strategy letter, we indicated the possibility of a correction in the stock market sometime in the first half of the year.1 While we were optimistic about the continuation of the bull market that we believe started in October 2022, we noted that corrections of 5-10% are normal in a bull market trend. On average, the S&P 500 Index has historically experienced a 10% correction at least once per year since 1929.2 During this current bull market, the S&P has risen approximately 70% from the October 2022 low through the end of 2024.2 During that 27 month stretch, the S&P 500 has only experienced one 10% correction which occurred in the fall of 2023.2

Although we didn’t necessarily wish for a correction in stocks earlier this year, we understood that bull markets don’t just go up in a straight line and corrections are a normal part of the process. Market corrections in long-term bull markets in the 10% to 20% range can help temper excessive investor optimism and bring stock valuations back down to more attractive levels. We believe that’s what’s happening now. As of the market close on Monday April 7, the S&P 500 Index had fallen 17.6% from its February 2025 all-time high. Year-to-date, the S&P 500 is down 14%.2 While we didn’t expect a decline in stocks of this magnitude in the first half of the year, we still view this recent downturn as a “healthy” correction in a long-term bull market. The market valuation of many stocks, in particular certain technology stocks, had become stretched by the end of 2024. With this recent correction, we believe equity valuations now look more attractive.

The recent decline in stocks is directly related to the Trump Administration’s announcement on Wednesday, April 2 of what it referred to as “reciprocal” tariffs on virtually all U.S. trading partners. Investors were expecting new tariffs but not to the extent of what the administration announced on April 2. Equity markets fell sharply on the Thursday and Friday following the announcement. For the two days, the S&P 500 fell a total of 10.5%.2 At one point during the trading session on the following Monday, the S&P 500 was down an additional 4.7% from Friday’s closing price but the S&P 500 recovered to end the trading session almost flat.

After the November elections, we felt that the incoming Trump administration and the Republican controlled House of Representatives and Senate, would move to put in place measures that would benefit both businesses and consumers. The Trump administration’s agenda included extending the 2017 Tax Cuts and Jobs Act (which expires at the end of 2025), implementing broad-based regulatory reform, dealing with illegal immigration, reducing the flow of fentanyl into the U.S., addressing the growing government budget deficit, and implementing tariffs to achieve fairer trade with our trading partners. We believed this pro-growth agenda would have a positive impact on the economy and the U.S equity markets although it would not be without “growing pains.”1 We also wrote in our letter that “aggressive new tariffs could set off a trade war with other countries which could negatively impact the global economy.” We added that increased tariffs would “likely create volatility and economic uncertainty.” In our view, that is exactly what has happening since the April 2 tariff announcement.

The speed of the implementation of the Trump administration’s agenda, especially on the issue of trade, is causing significant disruption in the business community. It appears that many business owners and corporate executives are holding off on plans to expand operations and hire new employees until there is more clarity on the nature

and impact of tariffs on their businesses. In addition, consumers are growing more concerned about how the new Trump policy measures will impact their pocketbooks. This is reflected in the recent drop in consumer confidence for the economy to the lowest level since January 2021, according to the latest survey from The Conference Board.4 Consumers have been cutting back on spending until they have more confidence that their jobs are more secure and inflation will not increase significantly due to higher tariffs.

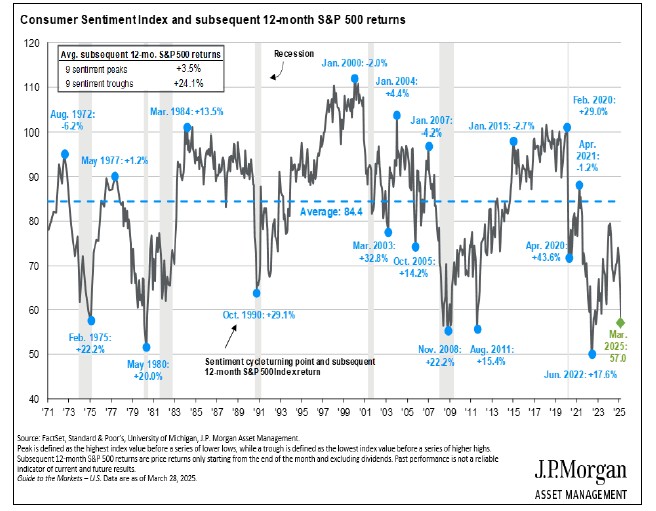

Another popular consumer sentiment survey, done by the University of Michigan, was revised lower in March to 57 points, down from the December level of 74 points.5 This is the lowest level for the index since June 2022. However, this is not all bad news. The index has frequently signaled turning points for the stock market as indicated in the chart to the left. The average return for the S&P 500 Index for the 12 months subsequent to a trough level in the sentiment index is 24.1% going back to 1971. Of course, we may not be at a cycle low for the sentiment index just yet. It has been lower three times  since 1980. Nonetheless, we believe there is a reasonable chance that consumer sentiment is nearing a trough for this cycle and will begin to improve over the next few quarters as many of the Trump administration policies take effect and the uncertainty around budget cuts and trade policy subsides.

since 1980. Nonetheless, we believe there is a reasonable chance that consumer sentiment is nearing a trough for this cycle and will begin to improve over the next few quarters as many of the Trump administration policies take effect and the uncertainty around budget cuts and trade policy subsides.

In the near term, the deceleration of both business and consumer spending is putting downward pressure on economic growth. In light of this, many economists have raised their probabilities of a recession for the U.S. economy this year. Adding fuel to the recession speculation, is the recent Atlanta Fed GDP estimate for the first quarter of 2025 of a negative 2.8%.6 But when you drill down into the details of their estimate, you find that the negative number is mainly due to the large trade deficit that they are projecting for the first quarter. We saw this same situation occur in 2022 when GDP was negative for the first two quarters of the year because of a large trade deficit and first quarter inventory build-up. GDP rebounded enough in the last two quarters of 2022 that the full year GDP came in at a positive 1.94%.7 While the Atlanta Fed’s GDP estimate is concerning for investors, it does not necessary signal that a recession is on the horizon for the U.S. economy.

We agree that the risk of a recession has increased with the implementation of the Trump administration tariffs. However, we believe the resilience of the U.S. economy will allow us to avoid an outright recession this year. Over the past five years, the U.S. economy has been hit with a global pandemic that killed millions of people and virtually shut down the entire global economy for several months, it experienced unusually high inflation that was exacerbated by a spike in energy costs caused by the start of the war in Ukraine in February 2022, and the economy

was burdened by an aggressive tightening of U.S. monetary policy by the Federal Reserve in 2022 to combat the inflation problem. Throughout that difficult five-year period, the economy grew by a total of 12.1%, including a small decline in GDP in 2020 of 2.2%.7 In our view, the U.S economy will be able to withstand the negative impact of the new tariffs. We see the Trump administration’s efforts to reduce government regulations on businesses, the extension of the 2017 tax cuts as well additional tax cut measures which should be passed by Congress this year, and the recent decline in interest rates, all working to offset the drag the new tariffs may have on the economy. Our base case remains, no recession this year, and for the U.S. economy to grow at a low single digit rate for 2025.

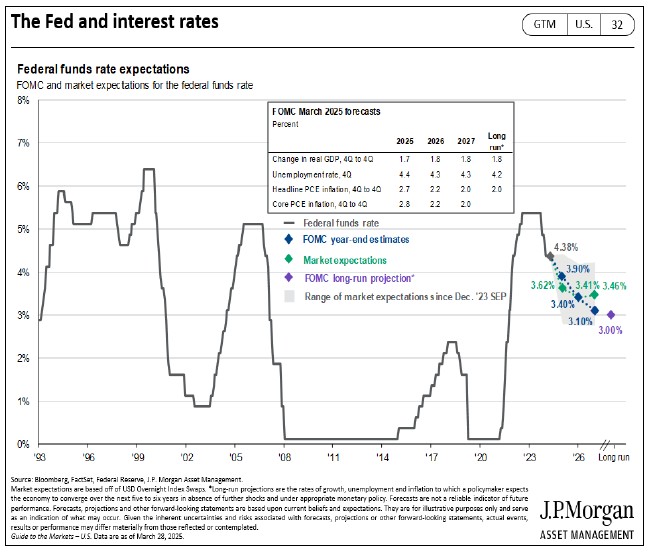

The Federal Reserve (Fed) could play an important role in how the economy deals with the negative economic impact of tariffs and budget cuts. The Fed’s policy committee that implements monetary policy, the Federal Open Markets Committee (FOMC), lowered the fed funds rate three times in the second half of 2024 by a total of 1%. Since the beginning of 2025, the FOMC has held the fed funds rate steady in their first two meetings of the year and indicated that the committee needs further clarity on how tariffs will impact both inflation and employment before considering further rate cuts. The chart to the right shows both the FOMC’s and the market expectations for the fed funds rate. The current level of the fed funds rate is an average of 4.38%. The expectation is for the rate to be cut three times in 2025 by .25% each. However, the number of cuts for 2025 could increase if the economy weakens significantly in the first half of the year. Typically, in periods of financial and economic weakness, the Fed would lower interest rates to help stimulate the economy.

The current negative sentiment about the economy and the impact of broad-based tariffs can leave investors very worried and even cause investors to reduce equity positions. While the “tariff tantrum” we are experiencing in the financial markets may persist for a while longer, we believe it is important to try to look past the near-term economic uncertainty and market volatility and focus on the longer-term picture where we see tremendous opportunity for growth. In our view, the U.S. remains the best place in the world to invest capital. We believe our constitutionally based government and judicial systems, the strength of our military power, the depth and liquidity of our financial markets, and our free-market-based economy, creates a very attractive environment for investors to put their capital to work. This “exceptionalism,” a term many have used to describe the U.S., is driving billions of dollars of capital investment into the U.S. economy, especially since the most recent federal

elections. U.S. companies have already begun the process of moving manufacturing facilities that they had moved offshore over the past 20 years back to the U.S. In addition, foreign companies have been building manufacturing facilities in the U.S. for years and are looking to accelerate that process, particularly in light of potential higher tariffs on goods they export to the U.S. We believe this activity will lead to a manufacturing renaissance in the U.S. over the next several years and will help to accelerate overall economic growth.

We believe the future looks very bright for the U.S. economy and financial markets. Of course, the road to prosperity will have its bumps and detours as we are experiencing currently. We feel that the economic uncertainty and the recent volatility of the U.S. financial markets will likely remain for the near-term until there is more clarity on the economic impact of President Trump’s agenda, especially his trade policies. However, in the second half of 2025, we believe the tariff issue will be mostly resolved and the focus of investors will shift to the positive impact of the deregulation efforts, progress on cutting the government deficit, and tax reduction through the extension of the 2017 Tax Cuts and Jobs Act as well as new tax relief. We also see overall U.S. employment remaining healthy and an acceleration of both business and consumer spending in the back half of the year. If we are correct, these positive developments could drive stock prices higher as investors become more positive about the U.S. economic outlook.

In closing, we recognize that the current situation in the financial markets can be both frustrating and stressful for our clients. Our recommendation is to remain patient and hold current allocations where appropriate. Tactical portfolio adjustments like shifting cash reserves to stocks could be considered depending on the circumstances. We believe the key to navigating through highly uncertain and volatile investment environments like the one we are in, is to be diversified through prudent asset allocation.

As always, we greatly appreciate your trust and confidence in us and we will continue to work to keep you informed of economic and financial market developments.

Your Trinity Capital Management Team

TCM Tyler, TX Location

821 ESE Loop 323, Suite 100

903-747-3960

Webite:www.tcmtx.com

Footnotes*

1 TCM Investment Outlook & Strategy, January 2025. https://www.tcmtx.com/blog

2 Thompson One charts

3 https://fiscaldata.treasury.gov/americas-finance-guide/national-deficit/

4 CNN article, “Consumer Confidence Plummets to the Lowest Level Since January 2021.” March 25, 2025

5 https://tradingeconomics.com/united-states/consumer-confidence

6 https://www.atlantafed.org/cqer/research/gdpnow

7 https://fred.stlouisfed.org/series/GDPC1

* To view the footnote links, press and hold the Ctrl key on your keyboard, hover over the link and left click your mouse.

Investment products and services are offered through Wells Fargo Advisors Financial Network, LLC (WFAFN), Member SIPC, a registered broker-dealer and separate non-bank affiliate of Wells Fargo and Company. Trinity Capital Management, LLC is separate entity from WFAFN.

Stocks offer long-term growth potential, but may fluctuate more and provide less current income than other investments. An investment in the stock market should be made with an understanding of the risks associated with common stocks, including market fluctuations. Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuation, political and economic instability, and different accounting standards. This may result in greater share price volatility.

The opinions expressed in this report are those of the author(s) and are not necessarily those of Wells Fargo Advisors Financial Network or its affiliates. The material has been prepared or is distributed solely for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy.

Wells Fargo Advisors Financial Network is not a legal or tax advisor. Consult your tax advisor or accountant for more details regarding your specific circumstance.

Investing in fixed income securities involves certain risks such as market risk if sold prior to maturity and credit risk especially if investing in high yield bonds, which have lower ratings and are subject to greater volatility. All fixed income securities may be worth less than the original cost upon redemption or maturity. Yields and market value will fluctuate so that your investment, if sold prior to maturity, may be worth more or less than its original cost. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment. Income from municipal securities is generally free from federal taxes and state taxes for residents of the issuing state. While the interest income is tax-free, capital gains, if any, will be subject to taxes. Income for some investors may be subject to the federal Alternative Minimum Tax (AMT).

Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns nor can diversification guarantee profits in a declining market.

S&P 500 Index: The S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market value weighted index with each stock's weight in the Index proportionate to its market value.

Index return information is provided for illustrative purposes only. Index returns do not represent investment performance or the results of actual trading. Index returns reflect general market results, assume the reinvestment of dividends and other distributions and do not reflect deduction for fees, expenses or taxes applicable to an actual investment. An index is unmanaged and not available for direct investment.

Past performance is no guarantee of future results and there is no guarantee that any forward-looking statements made in this communication will be attained.

Compliance Tracking Number: 10082026-7834249.1.1