Stephen M. Mills, CIMA® Partner

Chief Investment Strategist

Market Volatility Amid Geopolitical Uncertainty

Global equity markets started the year with strong momentum. The S&P 500 Index traded near all-time highs during the first two months, supported by solid earnings growth and generally positive investor sentiment. That changed suddenly in late February after military escalation involving Iran, which triggered a sharp but temporary market sell-off. The S&P 500 fell about 7–8% immediately afterward, then partially rebounded as investors reassessed the likelihood of a limited conflict.1

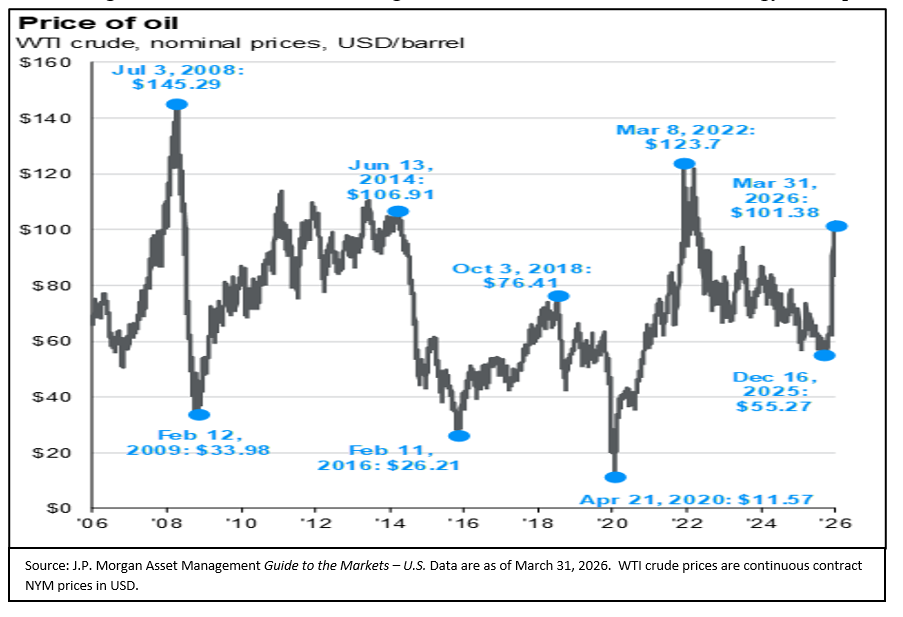

The geopolitical escalation has ha d a pronounced impact on energy markets. Approximately 20% of global oil supply flows through the Strait of Hormuz, making it one of the world’s most critical energy chokepoints. Disruptions in the region have pushed crude oil prices sharply higher, with West Texas Intermediate (WTI) rising from the mid-$50s earlier this year to near $100 per barrel, as shown in the adjacent chart. A sustained elevation in oil prices introduces downside risks to global growth. Higher energy costs, such as $4-per-gallon gasoline, can pressure consumer spending, increase businesses' input costs, and weigh on overall economic activity.

d a pronounced impact on energy markets. Approximately 20% of global oil supply flows through the Strait of Hormuz, making it one of the world’s most critical energy chokepoints. Disruptions in the region have pushed crude oil prices sharply higher, with West Texas Intermediate (WTI) rising from the mid-$50s earlier this year to near $100 per barrel, as shown in the adjacent chart. A sustained elevation in oil prices introduces downside risks to global growth. Higher energy costs, such as $4-per-gallon gasoline, can pressure consumer spending, increase businesses' input costs, and weigh on overall economic activity.

However, historical precedent shows that such shocks, while disruptive, are often temporary. During the 2022 Russia–Ukraine conflict, oil prices surged, and equity markets declined significantly. The price of a barrel of WTI rose from the low 90s to over $120, with gasoline prices briefly reaching $4 per gallon. The S&P 500 Index fell about 18% from late February, when Russia invaded Ukraine, to the end of September. Growth slowed temporarily but picked up again as energy prices normalized and financial conditions stabilized. Additionally, during that period, the Federal Reserve was raising interest rates, which may have contributed to the decline in stock prices. The U.S. economy demonstrated remarkable resilience during that turbulent year. We believe the same will be true this year, even if the war continues for several more months and oil prices remain high for an extended period.

Although we might see a slight deceleration in economic growth during the first two quarters, we believe the U.S. economy can withstand the negative effects of higher oil prices this year. As shown in the nearby chart, household spending as a percentage of after-tax income has fallen from a peak of 8.1% in May 1980 to 3.4% as of January 2026. This eases the financial burden on consumers from a temporary spike in energy costs. Also, thanks to the personal income tax cuts included in the One Big Beautiful Bill passed in July 2025, consumers are expected to receive an estimated $200 billion in tax refunds over the next few months. Importantly, consumer spending still accounts for nearly 70% of U.S. GDP . While higher gasoline prices may create short-term pressures, the overall financial health of households suggests the economy can absorb these shocks without entering a prolonged downturn.

. While higher gasoline prices may create short-term pressures, the overall financial health of households suggests the economy can absorb these shocks without entering a prolonged downturn.

Corporate Earnings Growth & Investment

The basis of our positive equity outlook continues to be solid corporate fundamentals, as outlined below:

- The S&P 500 has delivered multiple consecutive quarters of double-digit earnings growth.

- Revenue growth has accelerated, driven by pricing power and sustained demand.

- Profit margins remain healthy, supported by operational efficiency and disciplined cost management.

- Cash flows remain strong.

- The S&P 500 reported its fifth straight quarter of double-digit earnings growth in the fourth quarter of 2025. Revenue increased by 9% year over year, marking the strongest growth since 2022.2 FactSet's recent research report projects that S&P 500 earnings will increase by 13% in the first quarter of 2026, with full-year growth expected to be between 14-15%.2 This level of earnings growth supports higher equity valuations, especially once geopolitical uncertainty subsides. With double-digit earnings growth, corporate finances are as strong as they've been in many years. Cash flow is healthy, and debt levels are lower. This allows companies to invest capital to expand operations and enhance efficiency. One of the key drivers of future economic growth is the rapid expansion of AI-related capital investment. The so-called big tech “hyperscalers” (in

cluding Microsoft, Alphabet, Amazon, Meta, and Oracle) have collectively committed to spending $600 to $700 billion on AI investments in 2026.3 These companies are allocating this capital due to increased demand for cloud services and AI technology adoption. As noted in the chart above, AI spending is estimated to be an additional $761 billion from these five major tech firms in 2027 and $802 billion in 2028.

cluding Microsoft, Alphabet, Amazon, Meta, and Oracle) have collectively committed to spending $600 to $700 billion on AI investments in 2026.3 These companies are allocating this capital due to increased demand for cloud services and AI technology adoption. As noted in the chart above, AI spending is estimated to be an additional $761 billion from these five major tech firms in 2027 and $802 billion in 2028.

These large technology firms are dedicating substantial resources toward:

- Data center infrastructure

- Advanced semiconductor and GPU deployment

- Cloud computing capacity

- Energy infrastructure to support increased computational demand

These investments are primarily funded by strong free cash flow generation, though some “creative financing” arrangements have raised concerns among investors. Investors are worried that these financing structures understate true financial risk. As a result, several hyperscalers saw significant share price declines in the first quarter.

But overall, this wave of AI capital expenditure could enhance productivity across the broader economy, strengthening long-term growth prospects.

Policy Developments: Tariffs and Trade

Recent policy developments have also contributed to a more optimistic economic outlook. A Supreme Court ruling in February found that certain tariffs imposed by the Trump Administration under the International Emergency Economic Powers Act (IEEPA) exceeded President Trump’s authority. As a result, those tariffs were lifted, and the duties collected earlier became eligible for refunds. The President quickly imposed a new 15% tariff under a different law. These tariffs are limited to 150 days unless Congress extends them. The Supreme Court decision significantly impacted tariffs, reducing the average rate from 15.9% (as of February 20, 2026) to 12% (by March 31). From an economic perspective, we view this development as a positive change. In our opinion, tariffs act as a tax on both businesses and consumers, and their partial removal helps decrease trade friction and supports economic activity.

Bottom Line

While near-term uncertainty remains high, especially regarding geopolitical developments, our overall outlook is positive.

We believe:

- The current volatility is a temporary disruption, not a permanent shift.

- The underlying bull market that started in late 2022 remains intact.

- Strong earnings growth, resilient consumers, and ongoing investment in AI infrastructure form a solid basis for continued economic expansion in the U.S.

- As geopolitical risks decrease, we expect equity markets to respond favorably, potentially with a quick recovery.

We are actively monitoring developments and will continue to assess how changing conditions affect portfolios. As always, our focus remains on long-term investment results rather than short-term market fluctuations.

If you have any questions or want to discuss your portfolio in more detail, please feel free to contact us.

Your Trinity Capital Management Team

TCM Tyler, TX Location

821 ESE Loop 323, Suite 200

Tyler, Texas 75701

903-747-3960

Webite:www.tcmtx.com

1 FactSet Market Watch Charting

2 FactSet Insight, March 27, 2026

3 Futurum, “AI Capex 2026: The $690B Infrastructure Sprint.”

To view the above links, press and hold the Ctrl key on your keyboard, hover over the link, and left-click your mouse.

Investment products and services are offered through Thurston Springer Financial, a registered broker-dealer and member of SIPC. Trinity Capital Management, LLC, is a separate entity from Thurston Springer Financial.

The opinions expressed in this report are those of the author(s) and are not necessarily those of Thurston Springer Financial or its affiliates. The material has been prepared or is distributed solely for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy.

Past performance is no guarantee of future results, and there is no guarantee that any forward-looking statements made in this communication will be attained.

Investing in fixed income securities involves certain risks, such as market risk if sold prior to maturity and credit risk, especially if investing in high-yield bonds, which have lower ratings and are subject to greater volatility. All fixed-income securities may be worth less than the original cost upon redemption or maturity. Yields and market value will fluctuate so that your investment, if sold prior to maturity, may be worth more or less than its original cost. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline of the value of your investment. Income from municipal securities is generally free from federal taxes and state taxes for residents of the issuing state. While the interest income is tax-free, capital gains, if any, will be subject to taxes. Income for some investors may be subject to the federal Alternative Minimum Tax (AMT).

S&P 500 Index: The S&P 500 Index comprises 500 stocks selected for market size, liquidity, and industry group representation. It is a market-value-weighted index, with each stock's weight in the Index proportionate to its market value.

Index return information is provided for illustrative purposes only. Index returns do not represent investment performance or the results of actual trading. Index returns reflect general market results, assume the reinvestment of dividends and other distributions, and do not reflect deductions for fees, expenses, or taxes applicable to an actual investment. An index is unmanaged and not available for direct investment.