Stephen M. Mills, CIMA®

Partner

Chief Investment Strategist

Brad Bays, CIMA®

Partner

PIM Portfolio Manager

Highlights:

- Fears of a banking crisis in the U.S. economy led to higher-than-normal volatility in the financial markets in the first quarter.

- The Federal Reserve may be soon approaching the point when they will pause interest rate hikes.

- Inflation pressures in the economy continue to subside.

- We continue to expect a mild-to-moderate recession for the U.S. economy in 2023.

Commentary

The stock and bond markets continued to experience higher than normal volatility during the first quarter of 2023. March was a particularly volatile month as a potential banking crisis unfolded with two large banking institutions forced to shut down operations by the FDIC (Federal Deposit Insurance Corporation) due to insufficient capital reserves to cover the deposit withdrawals.

Both the stock and bond markets reacted to the news, with stocks prices moving down sharply and bond prices for U.S. government-backed securities rising as investors flocked to the safest areas of the financial markets. The fear of contagion subsided quickly with the move by the FDIC to insure all deposits at the two failed banks. Investors reacted positively to the news driving stock prices back up. The broad-based S&P 500 Index ended the quarter with a gain of 7.5% including dividends.1 Most of the major bond indices were slightly higher for the quarter as well.

Although the financial markets appear to have shaken off the banking concerns for the time being, we believe the aftershocks of the two bank failures will likely be felt for several months as lending institutions potentially tighten loan standards and reduce lending in order to protect their capital base in case the stress to the banking system increases. If access to credit becomes more difficult for consumers and businesses, we believe the economy could suffer. Small business lending is particularly important for the U.S. economy since almost half of all U.S. workers are employed by small businesses according to a recent Forbes study. Banks with less than $10 billion in assets accounted for 43% of small business loans outstanding at the end of 2022, according to Rebel Cole, a professor of finance at Florida Atlantic University.2 By contrast, the 13 largest U.S. banks accounted for less than 23% of small business loans, much of which are credit card balances.2 We see this potential tightening of credit as another headwind for the U.S. economy for the next few quarters increasing the probability of a recession this year. In our TCM 2023 Investment Outlook & Strategy letter sent out in January of this year, we stated that we expected the U.S. economy would experience a “mild-to-moderate recession in 2023 lasting two or three quarters.” (See footnote 3 for a link to this letter) This continues to be our view.

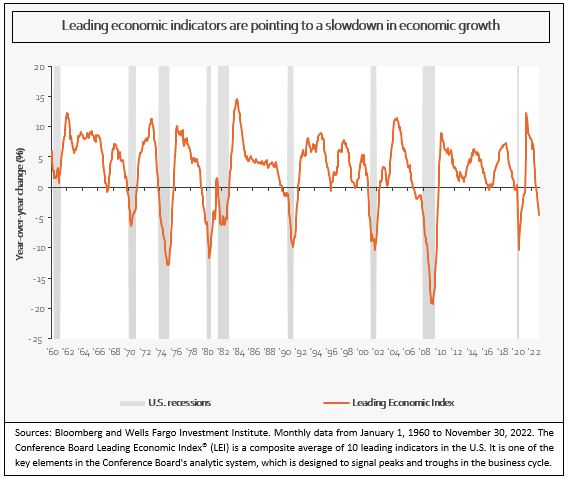

We see continued evidence in the data that U.S. economic growth is weakening. We believe the impact of the Federal Reserve’s (Fed) year-long monetary tightening strategy, initiated in March 2022, is beginning to negatively impact economic activity. Higher interest rates for both consumer and business loans tend to slow borrowing and curb spending. Although retail sales figures have been mostly positive for the past six months, we believe consumer spending will tail off over the next few quarters. Since consumer spending accounts for approximately 70% of U.S. output, weakness in retail sales could lead to a mild contraction in U.S. GDP in the second half of the year. Although the Fed believes it can bring down inflation without causing a recession, we have our doubts. From our viewpoint, the Fed’s aggressive monetary tightening strategy of rapidly raising interest rates along with reducing its balance sheet through quantitative tightening, will at the very least stall economic growth and at worst cause a moderate recession lasting a few quarters. We believe the odds of a so called “soft landing” for the U.S. economy have diminished with the latest Fed actions and the recent problems in the banking sector. The latest reading for the Index of Leading Economic Indicators (LEI), as reported by The Conference Board, fell for the 11th straight month and has reached a level that is often associated with a recession, as reflected in the above chart.4

We believe the recession risks and the concerns in the banking sector may cause the Fed to pause interest rate hikes soon. The most recent .25% rate hike by the Fed at its March meeting, moved the Fed funds rate up to the 4.75%-5% range.5 Based on the Fed’s statements and Chairman Powell’s post-meeting comments at both the December ’22 and March ‘23 meetings, we feel the Fed may hit the pause button on future rate increases as soon as their next meeting in May and then monitor inflation and economic data for a few months to see what impact its’ monetary tightening policy will have on both inflation and economic growth. Fed funds futures are now estimating a little over a 60% chance that there will be no rate hike at the Fed’s May meeting and a better than 90% chance of at least one .25% rate cut by year end.6

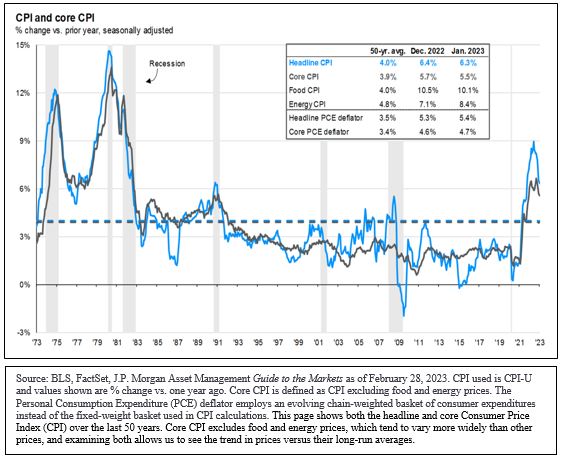

Inflation is another risk factor for the economy as it continues to run higher than normal at an annualized rate above 6%, as measured by the Consumer Price Index (CPI). However, the CPI has been trending lower the past several months. The adjacent chart of the CPI and core CPI illustrates the decline in prices since peaking in June 2022. Another key inflation indicator, the core personal consumption expenditures price index (PCE), one of the Fed’s preferred proxies for inflation, continues to move lower on a month-over-month basis according to data released by the Commerce Department for February which showed inflation rising 4.6% from a year earlier.7 We see inflation continuing to fall over the next few months as economic activity slows and key elements of the CPI like wages, housing costs, and food and energy prices continue to decline. If inflation continues to trend lower, this should allow the Fed to pause rate hikes and focus more on preventing further damage to the banking sector.

Despite the economic headwinds and problems in the banking sector, the global equity markets have shown resilience so far this year. As mentioned earlier, the S&P 500 Index gained 7% in the first quarter while the technology heavy NASDAQ composite surged 16.8%.1 The S&P 500 officially entered a bear market on June 16, 2022 went it fell 20% from its January 3, 2022 high. Since then, the S&P 500 has been in a trading range between the June ’22 lows of 3636 and the August ’22 highs of 4305. Currently, the S&P is trading nearer to the higher end of that range at 4129 as of April 21.1 We believe the S&P 500 will remain in this trading range for the next few months as investors assess the impact of the Fed’s monetary tightening policy on the economy.

Personally, we still favor high-quality, U.S. large company dividend stocks and growth stocks. We feel quality is the key to navigating this uncertain environment. That means holding stocks in larger companies that have strong balance sheets, positive cash flows, and favorable earnings forecasts. If we do enter a recession this year, we believe you want to own companies that can weather the storm and have the resources to take advantage of business investment opportunities. We still view small cap stocks as unfavorable at this time given the potential recession risks for the economy. Small businesses tend to be more sensitive to economic downturns and have fewer capital resources to weather a difficult economic environment. We are starting to become more bullish on international stocks. With China reopening from its Covid lockdown and Europe showing economic strength after a year-long recession, we feel now may be the time to add some exposure to these areas. Both valuations and growth prospects look attractive, in our view.

If you are looking to add fixed income, we also favor having a very high-quality portfolio. In particular, we would consider U.S. Treasury instruments along with high-quality corporate and mortgage-backed securities. Instruments that offer daily liquidity, as well as one-to-two-year CDs, are now offering attractive yields . We continue to favor a “barbell” approach for the fixed income portion of a portfolio where appropriate. The barbell consists of having a portion of one’s fixed-income portfolio invested in the very short end of the maturing spectrum in money funds and short-term fixed-income instruments (less than 2 years maturity) and another portion in longer-term maturity fixed-income instruments going out 10 to 20 years where appropriate. Although longer-term bonds carry a higher risk of fluctuation of principal as interest rates rise and fall, we believe the higher yields make them attractive currently. We see interest rates on longer-term fixed-income instrument trending lower this year, particularly if the U.S. economy inters a recession. Currently, the 10-Year Treasury note is yielding 3.6%.1 Whether it stays that high remains to be seen.

Another issue that investors may have to deal with and that could impact the financial markets is the upcoming budget process in the U.S. Congress and the need to raise the debt ceiling in order to continue funding government spending. The U.S. Government ran up against the $31.4 trillion debt limit in January of this year.9 Since then, the U.S. Treasury Department has been using special accounting measures to continue paying the government’s bill. These stop-gap measures will likely run out by this summer, forcing Congress to pass legislation to raise the debt ceiling. Currently, Democrats and Republicans in both houses of Congress are far apart on a new budget. If negotiations fall apart and the debt ceiling is not raised in time, the U.S. government would default on debt payments and other government obligations. Although such a default is unlikely since both sides of the political aisle understand the disastrous effect a default would have on the U.S. economy, Congress may take the issue right up to the deadline like they did in July of 2011, potentially negatively impacting the financial markets.

In summary, we see continued volatility for the financial markets until the Federal Reserve pauses rate hikes and more is known about the impact of the Fed’s monetary policy measures on inflation and the economy. We recommend maintaining a high degree of portfolio diversification and would use corrections in the financial markets to add to high quality stocks and bonds. We believe once we get deeper into the economic cycle and get more clarity on Fed policy, the Federal budget debate and the fallout from the recent bank failures, the stock market will become much more constructive.

As always, we greatly appreciate your continued trust and confidence in us and we will continue to work to keep you informed of economic and market developments.

Your Trinity Capital Management Team

Website:https://www.tcmtx.com/

Tyler TX Location

821 ESE Loop 323, Suite 100

Tyler, Texas 75701

903-747-3960

Footnotes

- Thompson Charts

- Wall Street Journal, “Small Banks Are Losing to Big Banks,” March 31, 2023

- https://www.tcmtx.com/blog/post/tcm-2023-investment-outlook-strategy-january-11-2023

- U.S. News & World Report, “Leading Indicators Fall Again in February, Signaling Recession on the Horizon,” March 17, 2023

- Wells Fargo Investment Institute Market, Federal Open Market Committee Meeting Key Takeaways, March 22,2023

- Dorsey Wight Daily Equity & Market Analysis, March 29, 2023

- Wall Street Journal, “Consumer Spending Growth Moderated in February and Core Inflation Eased,” March 31, 2023

- https://www.federalreserve.gov/newsevents/pressreleases/monetary20230312a.htm

- Wall Street Journal article, “Republican Budget Still Months Away, Complicating Debt-Ceiling Talks,” March 30, 2023

The indices presented in this material are to provide you with an understanding of their historic performance and are not presented to illustrate the performance of any security. Investors cannot directly purchase any index.

Stocks offer long-term growth potential, but may fluctuate more and provide less current income than other investments. An investment in the stock market should be made with an understanding of the risks associated with common stocks, including market fluctuations. Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuation, political and economic instability, and different accounting standards. This may result in greater share price volatility.

The opinions expressed in this report are those of the author(s) and are not necessarily those of Wells Fargo Advisors Financial Network or its affiliates. The material has been prepared or is distributed solely for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy.

Past performance is no guarantee of future results and there is no guarantee that any forward-looking statements made in this communication will be attained.

Wells Fargo Advisors Financial Network is not a legal or tax advisor. Consult your tax advisor or accountant for more details regarding your specific circumstance.

S&P 500 Index: The S&P 500 Index consists of 500 stocks chosen for market size, liquidity, and industry group representation. It is a market value weighted index with each stock's weight in the Index proportionate to its market value.

The Consumer Price Index (CPI) is a measure of the cost of goods purchased by average U.S. household. It is calculated by the U.S. government's Bureau of Labor Statistics.

Investment products and services are offered through Wells Fargo Advisors Financial Network, LLC (WFAFN), Member SIPC, a registered broker-dealer and separate non-bank affiliate of Wells Fargo and Company. Trinity Capital Management, LLC is separate entity from WFAFN.

CAR-0423-00748